|

| Pearl Primus: Please pretend this amazing picture is somehow relevant to coal shortages in the United Kingdom in 1947. |

Operation Sealion was the German "plan" for invading the United Kingdom in the summer of 1940, of which all that needs to be said, was said to me long ago by Mr. Kristiansen: "Shut up, kid." Millwrights may not know counterfactual history, but they've been around enough fights in their time to know what's what, best army versus best navy department.

However! Sealion was only a "plan" because the German navy and air force already had a plan, which was to place the entire United Kingdom under strategic siege and strangle it to death. On 21 August 1947, came irrefutable evidence that the strategy was working, as Britain abruptly cancelled the first steps already made to full convertibility from pounds sterling to dollars [pdf]. A year later, devaluation of the pound would signal Raeder and Goering's final victory. Three years after the end of the war.

|

| Good hustle! |

We know the basic outlines of the crisis: Britain was not earning enough dollars from exports to pay for imports from the hard currency dollar countries. In spite of the firm conventional wisdom that American manufacturing was hypertrophied at the end of the war due to the collapse of the competition, in fact Britain was going into debt buying mainly food and tobacco, while trying to pay for it by exporting machinery.* Britain would have been a great deal better off if it still had the robust coal exports that had enriched the nation in Victorian times, especially since a European coal shortage made for a robust market. It would also have been better off if it could have run its domestic manufacturing sector at full bore, but in the winter of 1947, a domestic coal shortage wreaked havoc on industrial production. One of the reasons for drastic action in August of 1947 was the fear that the misery of the previous winter would recur.

|

| Infant sitting on a coal wagon. Alex J. Robertson, The Bleak Midwinter |

Year

|

Output (millions of tons)

|

Exports

|

Employment(000s)

|

1870

|

110.4

|

11.3

|

350.9

|

1875

|

133.4

|

13.0

|

535.8

|

1880

|

147.0

|

17.9

|

484.6

|

1885

|

160.8

|

22.7

|

520.6

|

1890

|

181.6

|

28.7

|

632.4

|

1895

|

189.7

|

31.7

|

700.3

|

1900

|

225.2

|

44.1

|

780.1

|

1905

|

236.1

|

47.5

|

858.4

|

1910

|

264.4

|

62.1

|

1049.4

|

1913

|

287.4

|

73.4

|

1127.9

|

(Synthesis of two tables in M. W. Kirby, The British Coalmining Industry, 1870--1946: An Economic and Political History. I seem to have cropped the page numbers. Oh, well, good enough for blog work!)

It's perhaps no wonder that when Stanley Jevons considered "the coal question" in 1865, it was in terms of an exponential growth curve of coal production, tracking exponential growth in population, imports, and exports. According to Jevons, even Britain's estimated reserves of ninety billion tonnes of coal(!) would soon run out, after which civilisation would collapse, leaving the last survivors, etc, etc.

Such a stupid movie. But global warming, so relevant.

Since my "research" for this post consisted of going through a couple of open shelves in the HD9954 range in the Koerner Library this afternoon, it won't surprise that my copy of Jevons is a reprint of the 1900 reprint edition, which has to defend Jevons at the failure of his extrapolated exponential curve to come true. The singularity never happens, not even in the Nineteenth Century.

That being said, Jevons extrapolated his curves to infinity in 1865, before the chart above even begins. It might not show exponential increase, but it very definitely shows increase. Kirby holds the employment statistics for page over, as one way of showing that the industry isn't expanding because it is improving its total factor productivity or anything like that. That, in itself, is a contribution to a long-ago argument. I can only wonder how long Britain is going to be able to keep 1.1 million men working in the coal fields. If that's the only way that Britain can pay for all those imports, you begin to wonder if Corn Law Repeal was a good idea, after all.**

Jevons was wrong in another way:

|

| From Neil K. Buxton, The Economic Development of the British Coal Industry: From Industrial Revolution to the Present Day, 166. |

For all of Geoffrey Crowther's whining about the industry's failure to ever again reach the peaks of 1913, you could easily miss the point that the years between the wars were ones of managing decline and a chronic surplus of coal. As only too many authors are willing to explain, the major problem was deemed to be foreign, low-cost competitors; cost control was therefore vital, and the main cost was labour. It followed that labour costs had to be reduced, and, in the face of downward stickiness in wages, that could only be achieved by chronic underemployment in the coalfields, which duly occurred. I am not going to go too far in blaming the employer in this. They would certainly not have chosen the consequent aging of the workforce, as employees with seniority held on to good places while young, would-be entrants were discouraged into leaving the industry. At least, this is the process I infer from the makeup of the workforce during World War II. I do blame the employer for failing to see and intervene in this natural process. But what were they going to do? The oversupply seemed chronic, rationalisation impossible.

|

| Very substantial parts of the United Kingdom lie over a well-preserved, heavily forested Carboniferous (Devonian to early Permian) landscape. Just how much is unclear, as coal exploration can be expensive, and coal seams below about 1000 meters are of strictly academic interest. |

Brave talk about closing inefficient pits and moving labour around runs hard into the extensive nature of the industry, and the relative immobility of early 20th Century British work forces. Faced with the threat of widespread social collapse, and the likelihood that displaced coal miners would leave the industry, rather than moving into new coal mining villages in other regions of the country, subsequent governments could only dither and hope (and build Royal Ordnance Factories, when came the time).

For its part, industry responded with what M. W. Kirby calls "business collectivism," and The Economist calls "cartelism," in which market-sharing arrangements carved out room for existing players and attempted to manage reductions in capacity.

Traditionally, the industry's problems were seen to lie elsewhere. At first pass, tardy mechanisation, both in the form of a reluctance to adopt mechanised coal cutting, and motorised hauling underground was blamed for the problems of the industry. Leaving cutting aside for a moment, the figures traditionally cited here (which I lift from Ashworth and Pegg) are 80 locomotives underground in 1947; 7000 pit ponies still in use in 1950.

Drilling down (almost literally), it is pleaded that cutting and locomotives were ruled out by the antiquated and inefficient mines, which exploited narrow and sloping coal seams, and used acccess tunnels which followed the seams, rather than being driven straight through the associated strata. This sort of thing is Correlli Barnett's jam, and, for a change, he's not wrong. As Buxton points out, the ever-expanding demand for coal in the 1870--1913 period meant that many inefficient colleries were opened up. This gets a bit more complex in that what is, or isn't "inefficient" can depend on local transportation, which may make a nearby mine more valuable than it would otherwise be, and change the economic calculation when a new rail line or port is opened up, or when infrastructure becomes more efficient at, for example, clearing snow from the tracks. It also depends on markets for a particular product. Britain has either an unusually large proportion of good coal, or geology that lets people find it easily.

Once these apologies are made, however, it turns out that the premise is incorrect, that mechanised cutting actually expanded fairly quickly in the United Kingdom in the first half of the century, but that it failed to have the expected impact on coal raised per work shift, or on costs. Haulage was a different matter; and neither really impacted what seemed to be the most serious complaint against the industry, which was its failure to embrace mechanised American coalmining equipment when it became available.

This is the part where this post gets "surprisingly" technical. I was prepared to discover that the mechanisation story is a red herring. It's not, and in a very interesting way. Traditional coal mining mainly used what is called in America "room and pillar mining." This was the preferred method according to the most scientifically-minded British would-be coal mining reformers, and was the preferred method in the United States. Meanwhile, in the United Kingdom, and, crucially, in Germany, the rival "longwall" method was gaining ground in the interwar period. Obviously, according to the reformers, this was a retrograde step, but the obvious point here is that machinery suited to room and pillar techniques was not very suitable to longwall techniques.

The "reformers" were finally routed in the postwar era by the appearance of Gewerkschaft Eisenhuette Wesfalia's Panzerfoerderrer, the first "armoured face conveyor," which could run along the face of a longwall excavation, picking up the coal as it was cut and shunting it up the line to where it could be loaded into wagons. Once adopted in the Anglo-Saxon world, the armoured face conveyor defeated all objections to the concept of the face conveyor, and longwall mining took over from pillar and room mining. Here, we are on more familiar ground with the Barnett thesis, as it turns out that he has the direction of transatlantic flow of technological innovation reversed. Although he can be smug about the role of German engineering, and the reversal is, in any case, not going to last, as he is going to turn out be right, after all, again.

For the facts on American adoption of longwall mining, I turn to the American literature, and specifically to an outbreak of concern over stagnating productivity increases in the mid-90s, back before we just gave up on this problem after 2008 and entered the new age of "Waiting forGodot Elon Musk."

For its part, industry responded with what M. W. Kirby calls "business collectivism," and The Economist calls "cartelism," in which market-sharing arrangements carved out room for existing players and attempted to manage reductions in capacity.

Traditionally, the industry's problems were seen to lie elsewhere. At first pass, tardy mechanisation, both in the form of a reluctance to adopt mechanised coal cutting, and motorised hauling underground was blamed for the problems of the industry. Leaving cutting aside for a moment, the figures traditionally cited here (which I lift from Ashworth and Pegg) are 80 locomotives underground in 1947; 7000 pit ponies still in use in 1950.

Drilling down (almost literally), it is pleaded that cutting and locomotives were ruled out by the antiquated and inefficient mines, which exploited narrow and sloping coal seams, and used acccess tunnels which followed the seams, rather than being driven straight through the associated strata. This sort of thing is Correlli Barnett's jam, and, for a change, he's not wrong. As Buxton points out, the ever-expanding demand for coal in the 1870--1913 period meant that many inefficient colleries were opened up. This gets a bit more complex in that what is, or isn't "inefficient" can depend on local transportation, which may make a nearby mine more valuable than it would otherwise be, and change the economic calculation when a new rail line or port is opened up, or when infrastructure becomes more efficient at, for example, clearing snow from the tracks. It also depends on markets for a particular product. Britain has either an unusually large proportion of good coal, or geology that lets people find it easily.

Once these apologies are made, however, it turns out that the premise is incorrect, that mechanised cutting actually expanded fairly quickly in the United Kingdom in the first half of the century, but that it failed to have the expected impact on coal raised per work shift, or on costs. Haulage was a different matter; and neither really impacted what seemed to be the most serious complaint against the industry, which was its failure to embrace mechanised American coalmining equipment when it became available.

This is the part where this post gets "surprisingly" technical. I was prepared to discover that the mechanisation story is a red herring. It's not, and in a very interesting way. Traditional coal mining mainly used what is called in America "room and pillar mining." This was the preferred method according to the most scientifically-minded British would-be coal mining reformers, and was the preferred method in the United States. Meanwhile, in the United Kingdom, and, crucially, in Germany, the rival "longwall" method was gaining ground in the interwar period. Obviously, according to the reformers, this was a retrograde step, but the obvious point here is that machinery suited to room and pillar techniques was not very suitable to longwall techniques.

|

| Instead of looking at the illustations in Wikipedia, let's look at the ones in Ashworth and Pegg! |

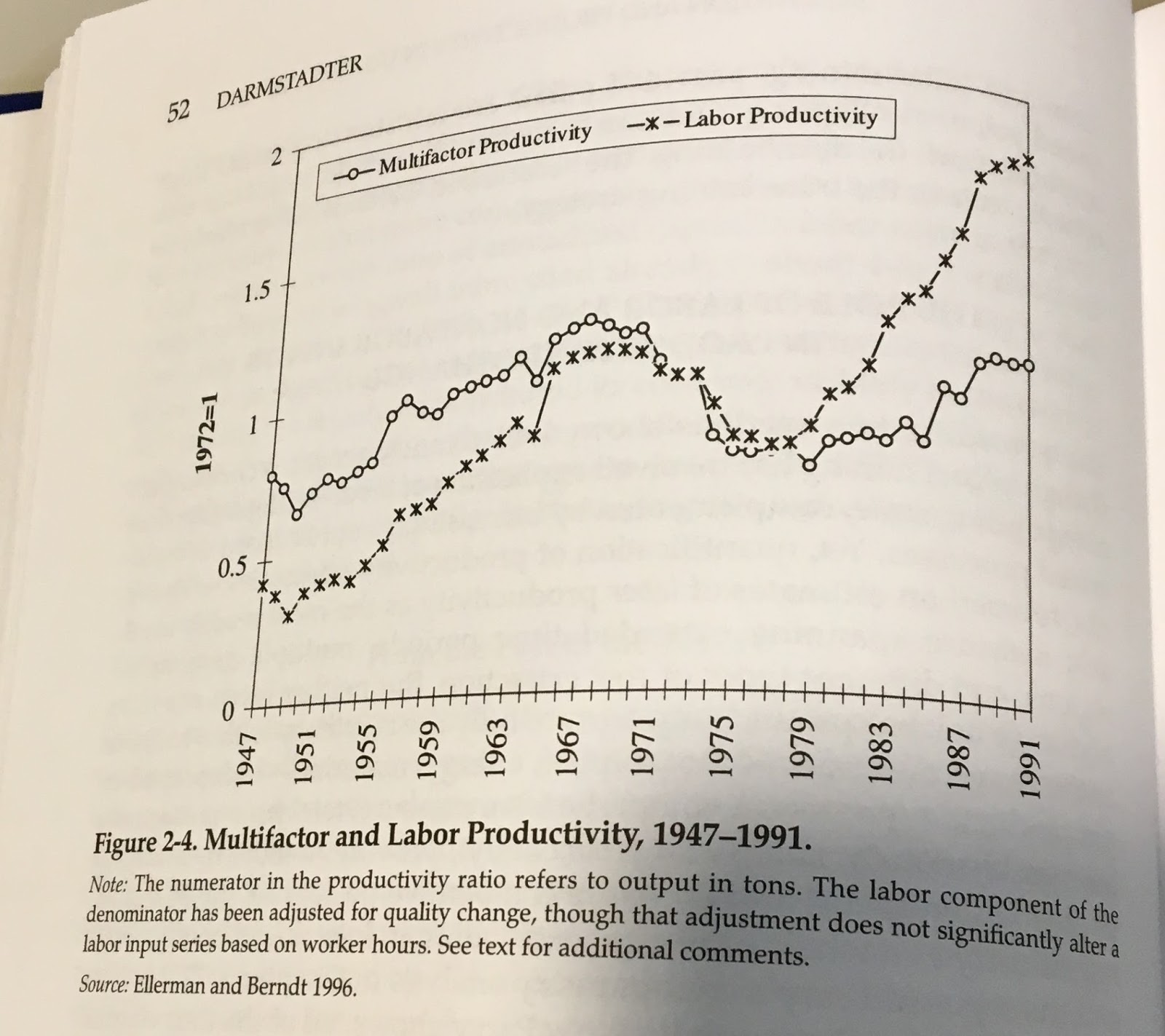

For the facts on American adoption of longwall mining, I turn to the American literature, and specifically to an outbreak of concern over stagnating productivity increases in the mid-90s, back before we just gave up on this problem after 2008 and entered the new age of "Waiting for

Here's a chart, which I lift from Joel Darmstadter's contribution to an edited volume from 1996. The volume editor is quite worried about the mid-70s dip in productivity, while Joel Darmstadter thinks it was a blip due to safety regulations or unions or something, and that the resumed upward trend of the 1990s shows that everything's all right, now. As I've already suggested, the trends of the last decade would suggest that his optimism was premature. Not to belabour the obvious, but the return of interwar secular stagnation indicates that we're not getting the productivity story quite right.

At this point, it would be as well to return to the story of longwall mining, and Correlli Barnett. Why was longwall mining advancing (that's a longwall mining pun!) during the interwar period, when it doesn't seem to be yielding higher productivities, and Americans have no time for it, and when the gurus of the industry have set their faces against it?

Because of an issue that hasn't come up, and doesn't seem to come up in these discussions, but which is central to the choice between longwall and pit-and-room mining: subsidence. Mines are holes underground, and, to the dismay of drow everywhere, holes underground really don't want to exist. There's a lot of weight on top of them, trying to make them not exist. Sometimes, that is good for coal mining, as when it compresses vegetable matter in to hard, firm bits of "coal." Sometimes it is not, as, for example, when it kills people in cave-ins, caused massive sinkholes above ground, and costs too much in pit props to keep things going.

It will be recalled that pit props are scarce in wartime Britain, due to the traditional supply from Norway being cut off (Good hustle, Erich, he said nonsarcastically), and Canada being far away. The return of peace is leading to a bit of an Indian summer for the pit prop loggers of the far Northwest in 1947, which we Pacific Coasters are not too proud to say "thank you," for, and "Can we have another?"

Alas, modern pit props are all technological and have hydraulic bits and plungers and stuff and are made of steel and rubber and such.

The final point, and it has to be a final point, since I should have already left for work, is that subsidence is the greater problem in a poorly-chosen colliery. So at first pass, it really does look as though it was all those "inefficient" pits and the Victorian over-expansion that is the central problem here. Correlli's right!

At this point, it would be as well to return to the story of longwall mining, and Correlli Barnett. Why was longwall mining advancing (that's a longwall mining pun!) during the interwar period, when it doesn't seem to be yielding higher productivities, and Americans have no time for it, and when the gurus of the industry have set their faces against it?

Because of an issue that hasn't come up, and doesn't seem to come up in these discussions, but which is central to the choice between longwall and pit-and-room mining: subsidence. Mines are holes underground, and, to the dismay of drow everywhere, holes underground really don't want to exist. There's a lot of weight on top of them, trying to make them not exist. Sometimes, that is good for coal mining, as when it compresses vegetable matter in to hard, firm bits of "coal." Sometimes it is not, as, for example, when it kills people in cave-ins, caused massive sinkholes above ground, and costs too much in pit props to keep things going.

It will be recalled that pit props are scarce in wartime Britain, due to the traditional supply from Norway being cut off (Good hustle, Erich, he said nonsarcastically), and Canada being far away. The return of peace is leading to a bit of an Indian summer for the pit prop loggers of the far Northwest in 1947, which we Pacific Coasters are not too proud to say "thank you," for, and "Can we have another?"

Alas, modern pit props are all technological and have hydraulic bits and plungers and stuff and are made of steel and rubber and such.

The final point, and it has to be a final point, since I should have already left for work, is that subsidence is the greater problem in a poorly-chosen colliery. So at first pass, it really does look as though it was all those "inefficient" pits and the Victorian over-expansion that is the central problem here. Correlli's right!

*

**Don't look at me like that; you're not the one who decided to read old numbers of The Economist for a hobby. At this point, if I read about law of gravity in From The Economist of 1847 feature, I at least think about jumping out the window to see whether James Wilson is having me on. But that's a silly hypothetical, because to do that, he'd have to go to the trouble of looking up what "the law of gravity" was, which would keep him at the office past noon.

"Surprisingly" technical? Read the BoE pdf on exchange controls and came away with the conclusion Keynes probably understood it but I didn't.

ReplyDeleteAs I understand it, the original idea was that British importers would buy American cotton with something (gold? credit?) and take it home to Britain. There, they would industrial revolution it up into underwear and socks to be stuffed into American Christmas stockings. The Americans would pay for that with dollars, which would be carried home to England, where no-one will take your foreign, funny money, so you take it to the Bank of England (if you want to write for The Economist, however, don't for God's sake say that. Say something like "window," or, better yet, "discount window," without defining what's being discounted against what.)

ReplyDeleteNow, the Bank of England has American dollars. So, say you are a big brewer/miller and want to buy some American grain. You borrow some pounds go to the Bank of England with your pounds and buy some dollars at the price that the Bank of England gives you (maybe that's where the "discount" in "window" comes in?).

[Cont] Note that the whole "gold standard" thing here gets a bit rubbishy, as the price of gold in American dollars is higher in London than in New York because reasons.

ReplyDeleteAnyway, you, the would-be American grain importer, now have American dollars, which you haul over to New York to buy your American grain with your American dollars, which you then take back to England where you sell your bread and beer and make tons of money. (In pounds.)

Ideally, out of this, the Bank of England ends up with a growing surplus of American dollars every year. These are now available to financiers, who might want to buy American farmland from the Fennimore Coopers, or railroad stocks from Leland Stanford. These properties will produce annual revenues (ideally -sorry about Governors of California, guys. If it's any consolation, eventually one of them will play governor with Linda Ronstadt and give us some fine hurtin' songs.) These will be taken back to London, and converted into pounds.

In the end, there's an ever-accumulating surplus of dollars in London, which is awesome, because every time you increase American grain production, it will get that much cheaper. Now, Norwegians might be induced to buy American grain. One way to do that is to do the hard work of developing the American lutefisk and whalemeat market. That's hard.

The other way, which is easy, is to export pit prop lumber to England, take the payment in pounds, and then go to the Bank of England and convert those pounds into dollars.

So everything is fine, give or take stream-of-consciousness blather about what "the market" thinks about the "discount rate" this week . . . Until America starts making its own socks and underwear, while meanwhile American grain gets so cheap that it begins to drive British grain off the market, and British grain imports start getting so extensive that people start eating so much grain that. . . I'd extend the thought to get to the point where "Virginia tobacco" is starting to appear as a serious issue in the books, but that era is just so strange to us that I'm not sure that I can.

ReplyDeleteAnyway, the upshot is WWII, by which time the world is importing so much American stuff, and America is importing so little foreign stuff, that the world's going to be in serious trouble if British investors start selling or even mortgaging all of that American farmland and those railroad equities. (Because sometimes they are stocks, and sometimes they are bonds, and God forbid that a real economics writer explain the difference instead of inventing a new word to include both categories of undefined things.)

So now England needs, or wants, grain and tobacco, and so on; and Norway needs grain, and tobacco, and so on; and England needs pit props. The trick is, there's just not enough dollars in London to pay for everything that everyone wants.

ReplyDeleteWhich means that England is at serious risk of not getting grain or pit props. So it sets up an American dollar account for Norway to draw on, in London. That's how many American dollars Norway gets to convert pounds into, to pay for American stuff.

But Norway isn't the only player here; they're just, you know, which makes them the right kind of people. There's also Uruguay, which can sell canned corned beef to London or to New York. It gets a crap price from New York, so it wants to sell in London. Fine, says London; here's your pound-denominated payment.

But we really want to pay our American loans, Uruguay says. Marines are terrible houseguests! Tough, says London. Try selling your corned beef in New York. Also, New York, while you're paying attention, can we have a huge line of credit in American dollars, just till we get back on our feet? Gladly pay you Wednesday for a hamburger today!

So New York says, fine. As long as Uruguay gets enough money to pay its American loans. And London says, okay, it can have enough to cover its corned beef deliveries, because we really need that corned beef.

So, on cue, about ten times as much corned beef as Uruguay has ever delivered before arrives on the London docks at one-fifth the price. To be converted into twice as many American dollars.

This is the game that the Labour Government shut down in August of 1947.

In writing like this, I've deliberately slighted Uruguay's concerns. It is getting stuck with pounds sterling when there's really not that much that Uruguay wants to buy in pounds sterling, and when it really, really needs dollars. It's also a game that is going to go on to the limits of the Bank of England's ability to control it until the whole line of credit is gone.

ReplyDeleteThat's why the Marshall Plan, with all its indirectness, seems like the solution. Whatever the proximate destination of the dollars being shipped out of America, it is going to pump enough American dollars into the world to correct the congenital world-versus-America balance of trade issue. Hopefully.

The discount window: this is about internal monetary policy, not about foreign exchange*. A central bank that operates a discount window offers short-term (overnight or one week) loans to commercial banks in cash, taking bonds as collateral. The discount on the face value of the bond is equivalent to a rate of interest.

ReplyDeleteAt the margin, the commercial banks can get liquidity from the discount window when they can't get it elsewhere. Therefore, if the central bank cuts the rate it charges at the window, lengthens the terms, or accepts more classes of bonds as collateral, banks can lend more money to the real economy and market interest rates fall. A couple of years ago, the European Central Bank really took this to an extreme by discounting assets with a term of several years under the so-called LTRO or Long Term Refinancing Operations, in an effort to influence long-term interest rates more.

Back In The Good Old Days, there was a whole lot of extra institutional complexity to how the Bank of England did this because it only dealt at the window with an intermediary layer of firms called discount houses, who then advanced credit to the banking sector.

*hard core economists would say there is no difference, but a) they're full of shit, b) there certainly is a difference if there are exchange controls in place, and c) the point of imposing exchange controls is precisely to run an interest rate internally that external capital flows wouldn't otherwise permit.

In the institutional setup you're talking about, the foreign exchange and sterling capital markets are linked when free payments are allowed, but divided when they are controlled.

ReplyDeleteIt's a good thing that at least Alex knows what he's talking about. . .

ReplyDelete